In a decision of 20 July 2017 in the case Marco Tronchetti Provera SpA e.a. v. Consob, the European Court of Justice ruled for the first time on the interpretation of article 5(4) of the Takeover Directive, which covers the possibility for the national supervisory authority to adjust the price of a mandatory bid. In this case, the Italian supervisory authority, the Consob, had decided to increase the price because it believed that there was collusion between the bidder and one of the sellers. This price adjustment was allowed by Italian takeover law, but the bidder believed that the Italian law violated the Takeover Directive, arguing that the criteria for a price adjustment were insufficiently clear. The Court of Justice ruled, however, that the concept of collusion that is used in Italian law as one of the possible justifications for a price adjustment is not necessarily too vague. This way, the Court further clarifies the competence of national legislators to regulate the fair price in mandatory bids.

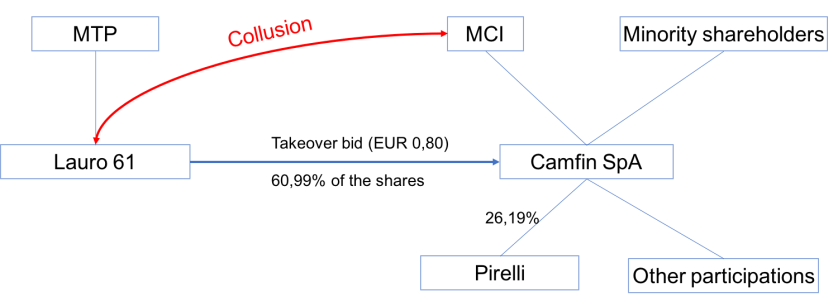

The facts of the case are important to understand the relevant legal issue. Marco Tronchetti Provera & C. SpA (MTP), an Italian company, had set up a subsidiary, Lauro 61 SpA, in order to acquire all of the shares of Camfin SpA, a holding company listed on the Milan Stock Exchange. Camfin held, amongst other participations, a participation of 26,19% in Pirelli & C. SpA.

The bidder Lauro 61 had acquired 60,99% of the shares in Camfin, after concluding transactions with many shareholders of Camfin, including Malacalza Investimenti Srl (“MCI”). Lauro 61 was thus required to launch a mandatory bid, as the threshold of 30% of the shares was crossed. In accordance with Italian law, the price in the mandatory takeover bid was EUR 0,80 per share, the highest price that was paid over the previous 12 months.

However, minority shareholders of Camfin complained with the Consob, which decided to increase the price of the mandatory bid. The reason for this was an agreement between (amongst others) MTP, Lauro 61 and MCI. Pursuant to this agreement, MCI agreed to sell its shares in Camfin to the bidders at a price of EUR 0,80 per share. But MCI also bought a participation of 6,98% in Pirelli from the bidders at a price of EUR 7,80 per share, even though the market value of those shares was EUR 8,00 per share. The Consob decided that the lower price for the Pirelli shares constituted an extra advantage for MCI, which should be reflected in an increase of the price of the mandatory bid to EUR 0,83 per share.

Indeed, according to article 5(4) the Takeover Directive, the price of a mandatory bid shall be regarded as equitable if it is equal to “the highest price paid for the same securities by the offeror, or by persons acting in concert with him/her, over a period, to be determined by Member States, of not less than six months and not more than 12 before the bid”.

However, the second paragraph of article 5(4) contains an exception to the “highest price paid rule”, laying down the conditions for a price adjustment, as well as some non-exhaustive examples: “Member States may authorise their supervisory authorities to adjust the price referred to in the first subparagraph in circumstances and in accordance with criteria that are clearly determined. To that end, they may draw up a list of circumstances in which the highest price may be adjusted either upwards or downwards, for example where the highest price was set by agreement between the purchaser and a seller, where the market prices of the securities in question have been manipulated, where market prices in general or certain market prices in particular have been affected by exceptional occurrences, or in order to enable a firm in difficulty to be rescued.” (own emphasis).

This possibility has been implemented in Italian law. Article 106(3)(d) of the “Decreto legislativo nr. 58” stipulates that the Consob can increase the bid price in a mandatory bid, if one of the mentioned circumstances are present, including the presence of collusion (“collusione”) between the bidder (or the persons acting in concert with the bidder) and one or more of the sellers. In the case at hand, however, it was not clear whether the parties to the side-agreement intended to collude (as mentioned by AG Wahl in his opinion).

In the case at hand, the Italian courts clarified that the requirement of collusion does not require the minority shareholders to prove an element of intent or fraud, even though this is required under the definition of “collusion” in other fields of law. The bidders and concerted parties argue that this interpretation of “collusion” is too vague and gives the Consob an unlimited degree of discretion, which violates the requirement in article 5(4) that the criteria for the price adjustment are “clearly determined”. Basically, this argument boils down to the argument against every anti-abuse rule (which article 5(4) clearly is): “it harms legal certainty”.

The Court of Justice struck down the arguments of the bidders. The Court agrees with the Advocate-General that the requirement that the criteria are clearly determined does not preclude member states from using abstract legal concepts, such as “collusion”. Here, the Court recognizes that every anti-abuse rule features some degree of open-endedness, which is necessary precisely to prevent circumvention of the rule.

Second, the Court ruled that the fact that a concept such as “collusion” has another meaning in other fields of law (such as for example in competition law), does not mean that it is not “clearly determined”. The Court leaves the final decision of whether the notion of collusion is sufficiently clear to the determination by the Italian court, “using methods of interpretation recognised by the national law”. But the wording of the decision seems to suggest that the Court does consider the Italian provisions sufficiently clear. This is contrary to the opinion of AG Wahl, who seemed to consider the fact that there were doubts on how the concept of collusion should be interpreted under Italian law as evidence that the provision was not sufficiently clear.

In conclusion, the decision of the Court of Justice provides a nice illustration of the provisions on price adjustments in mandatory bids. In essence, these provisions aim to ensure that minority shareholders receive an equitable price. In the case at hand, the bidders and one of the selling shareholders concluded a side-agreement, without any evidence that this occurred in bad faith. Nevertheless, the agreement did have an impact on the fairness of the price, so that a price adjustment was justified. The Italian rules provided this option, and the Court of Justice held that this was in accordance with the Takeover Directive.

This is good news for other European countries with similar rules. For example, under article 55 of the Belgian Takeover Decree, a price adjustment by the Financial Services and Markets Authority (FSMA) is possible when (1) some of the selling shareholders have agreed to “special obligations” (for example representations and warranties); (2) when additional economic benefits are awarded to some of the selling shareholders; or (3) when the market prices are not meaningful or when information has been made public that could give misleading signals about the shares. The second rule would allow for a similar solution as under the Italian rule that was the subject of the case. Similarly, under article 234-6 of the General Regulation of the French Authorité des Marchés Financiers (AMF), a price increase by the AMF is possible in case of a related transaction between the bidder and the selling shareholders (amongst other circumstances).[1]

In the United Kingdom, on the other hand, note 3 on rule 9.5 of the Takeover Code only contains a list of “circumstances which the Panel might take into account when considering an adjustment of the highest price”. In the Netherlands, the criteria are even vaguer: article 5:80b of the Financial Supervision Act simply states that the takeover price can be adjusted if this is necessary to reach an “equitable price” (“billijke prijs”), without giving further guidance.

One can wonder whether these legal regimes for price adjustments in mandatory bids are “sufficiently clear”, as required by the article 5(4) of the Takeover Directive. The decision discussed in this blogpost indicates that the Court of Justice does not take a very stringent view on this issue, as long as the interpretation of the provisions is clear under the methods of national law (which seem to allow room for further interpretation by national courts and supervisory authorities). Still, with an open-ended provision such as article 5(4) of the Takeover Directive, which is intended as an anti-abuse rule that ensures a fair takeover price, there is an inherent tension between achieving this objective and legal certainty. Only further applications of these rules can give more guidance on how this tension will be resolved.

PhD Candidate at the Jan Ronse Institute of Company and Financial Law, KU Leuven

[1] “Lorsque le prix mentionné au premier alinéa résulte d’une transaction assortie d’éléments connexes entre l’initiateur, agissant seul ou de concert, et le vendeur des titres acquis par l’initiateur au cours des douze derniers mois.”

2 thoughts on “New ECJ ruling on price adjustments in mandatory bids in case of collusion”